Issue #013 named the signpost and said the regime’s direction depended entirely on oil duration. Issue #014 opens with the verdict: Path B confirmed. Brent settled Friday at $92.69, its biggest weekly gain since April 2020. Hormuz tanker traffic is near zero. WTI’s 35.6% weekly surge is the largest in the futures contract’s history dating back to 1983. As of Sunday evening, futures are pointing to a Monday open in the $105-110 range.

But none of that is what this issue is about. Last week happened. What matters now is what happens next and this coming week contains the single most important data release the framework will see in all of 2026 so far.

Wednesday’s CPI is the inflation baseline before the oil shock fully transmits. Friday’s Michigan Consumer Sentiment is the Fed’s leash, if 5-year inflation expectations break higher, the policy trap becomes explicit. And every morning, Brent and tanker traffic data will tell you more about the regime than any official statistic.

Regime Check: Stagflation

The dashboard scores where we’ve been. The week ahead tells us where we’re going.

For weeks the framework scored Neutral/Chop while the signposts accumulated. That regime is now behind us. The pillar moves are directionally clear even if the data catching up to real-world conditions takes a few more weeks.

On the Limits of This Week’s Formal Scores

The ISM surveys, NFP and CPI pipeline data all reflect the pre-shock economy, collected before February 28. The formal pillar scores below represent the starting position as the oil shock begins to transmit. They are a floor, not a ceiling. Expect the scores to move further and faster as March data arrives.

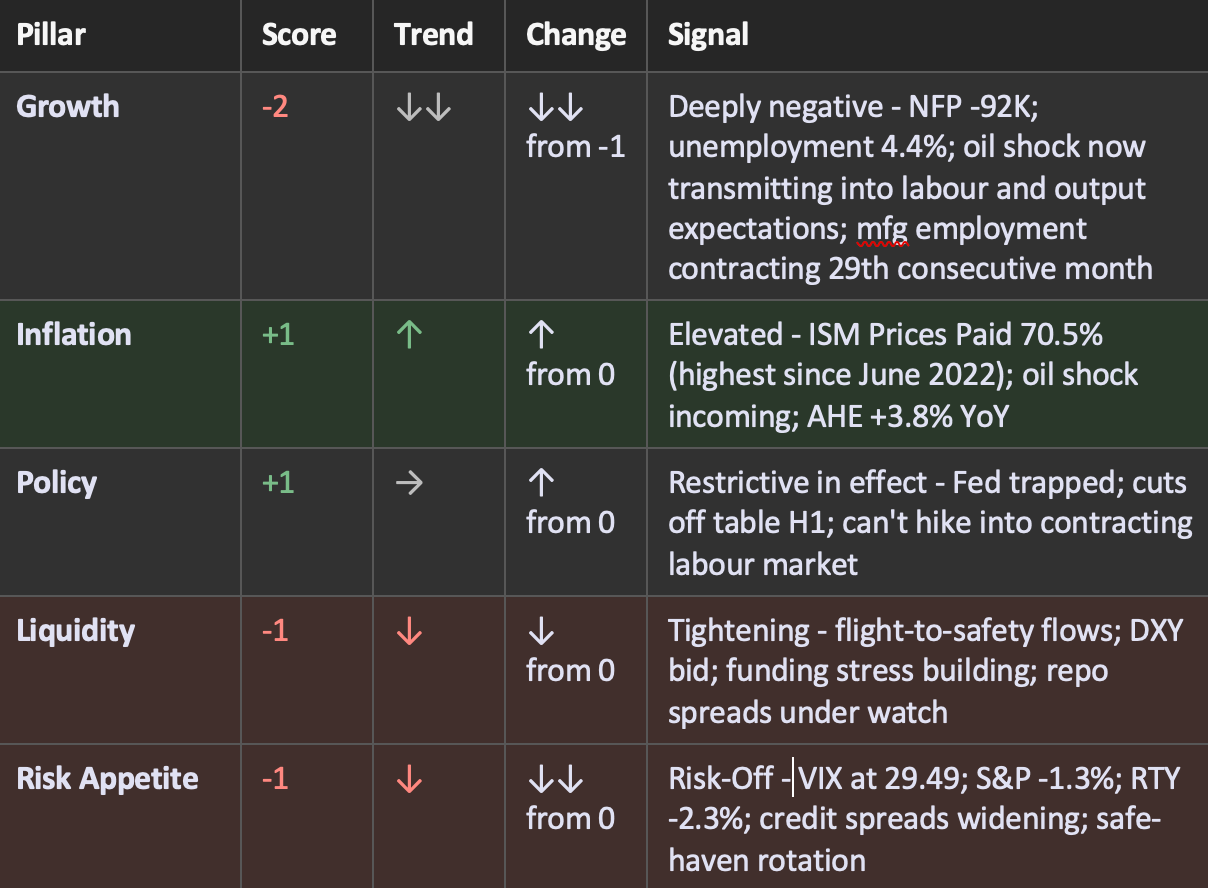

Current Regime: Stagflation | Aggregate Score: -3 | Modifier: Confirmed | Conviction: Elevated

The regime has moved to Stagflation. Growth is deeply negative (-2), Inflation elevated (+1), Policy trapped (+1), Liquidity tightening (-1), Risk Appetite deteriorating (-1). Aggregate score: -3. The Tearsheet scores this unambiguously, the combination of an oil supply shock arriving into an economy already showing deteriorating employment and sticky inflation has crossed the threshold. This is not a border call. Growth expectations have moved sufficiently negative and the inflation pipeline is sufficiently loaded, to lock the Stagflation quadrant.

The December scare was transient: year-end plumbing stress, a single hot PCE print, quickly reversed. This is structurally different. A supply-side energy shock has arrived into an economy where ISM Prices Paid was already at 70.5, its highest since June 2022, seventeenth consecutive month of rising input costs, collected entirely pre-strike. The inflation pressure was building before the oil shock. The oil shock is acceleration.

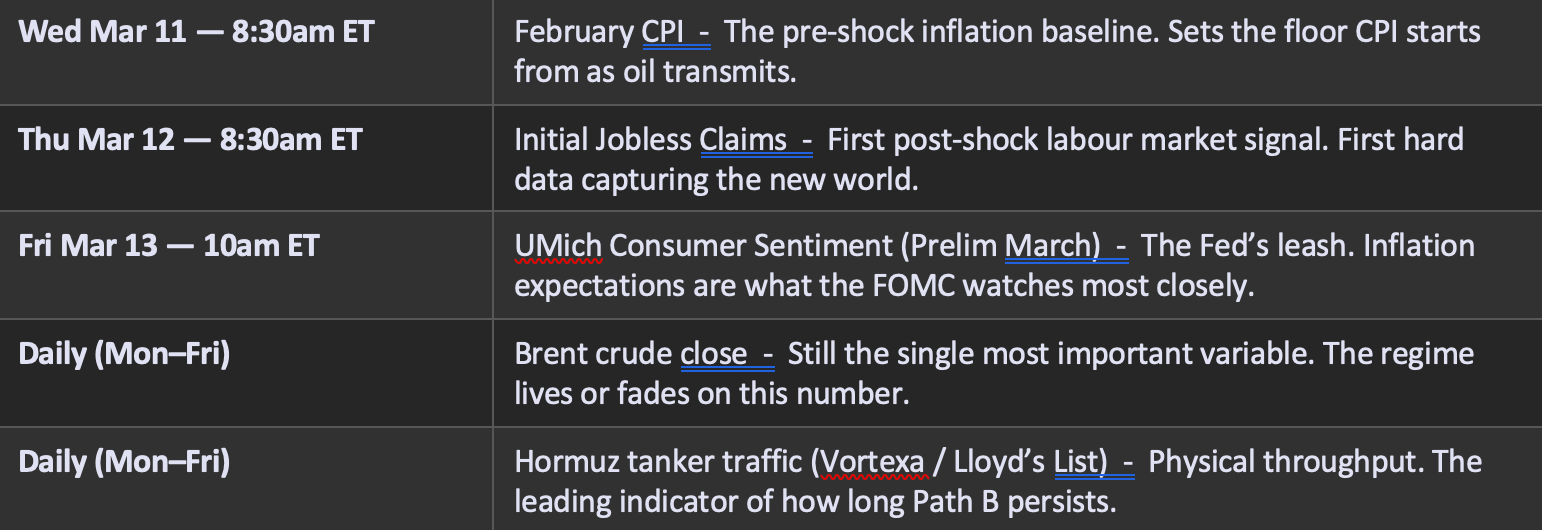

The Week Ahead: Why This Is the Most Important Setup of 2026

Three releases this week will materially define the regime trajectory for the coming month. They arrive in a specific sequence, and the sequence matters. Here is how to think about each one before it lands.

Wednesday: February CPI - The Most Important Print of the Year

January CPI: +0.2% MoM, +2.4% YoY. Core: +0.3% MoM, +2.5% YoY. That is the starting point.

February CPI will be released Wednesday morning. This print has a unique analytical significance that goes beyond the usual monthly data point: it is the last clean CPI read before the oil shock begins to flow through consumer prices. Whatever it shows is the base from which the inflation repricing begins.

The January read looked constructive on the surface. But the sub-components told a more complicated story. Shelter running above 4% annually. Services inflation sticky. Core PCE at 2.9% with a 0.4% monthly print, the inflation pipeline was refilling. The disinflation narrative that defined the second half of 2025 had already lost conviction before a barrel of oil moved.

Three scenarios, each with a different regime implication:

Scenario A: Hot (+0.4%+ MoM, Core +0.3%+)

The scenario the framework leans toward, given sticky shelter, Services Prices Index at 63.0, and a 0.4% January core read. A hot February print (before oil has transmitted) pushes the Inflation pillar toward +2 and tips the regime from Late Cycle toward the Stagflation border in a single print. Watch the 2Y yield: a move above 4.5% signals the market fully repricing the cut timeline.

Scenario B: In Line (+0.2-0.3% MoM)

Not reassuring in the current context, it simply confirms the starting position is where we thought it was, and the oil shock adds to that from here. The regime call is unchanged. Attention shifts immediately to Friday’s Michigan expectations.

Scenario C: Soft (+0.1% or below)

The least likely outcome. Any undershoot provides brief relief but interpret it carefully: February’s energy CPI was captured with Brent at $70-73. March CPI (released mid-April) captures $85-93+ oil. This week’s print is the baseline, not the peak.

The CPI Framework Watch

The number itself matters less than the trajectory it implies. With Brent at $92.69, ISM Prices Paid at 70.5%, and core PCE already at 2.9%, the direction of travel is not in question. The February CPI tells us the starting altitude before we begin climbing.

Thursday: Initial Claims - The First Post-Shock Labour Read

NFP shed 92,000 jobs in February, confirmed Friday. The consensus had expected a small gain. That print was the third job loss in five months and reflected a labour market that was already softening before the strikes.

Thursday’s initial jobless claims will be the first data point capturing the week of March 2, the first full trading week under the oil shock. This is the earliest hard signal of whether the energy disruption is producing layoffs.

The four-week moving average of claims has been running in the 220-230K range. Here is what to watch for:

• Below 230K - labour market holding. The shock is not yet visible in hiring/firing decisions. This is the most likely outcome given the one-week lag in claims data.

• 230-260K - early stress signal. Some industries (airlines, logistics, consumer-facing services) beginning to react. Not alarm, but the direction is confirmed.

• Above 260K - early deterioration. Growth pillar pressure intensifies. The argument that services expansion (ISM 56.1%) buffers the shock starts to erode.

Context: the healthcare strike that distorted February NFP (28,000 jobs lost) ended February 23. That effect should normalise in claims data from here. Any jump above 240K that cannot be attributed to a specific sector event is a genuine deterioration signal.

Friday: Michigan Sentiment - The Fed’s Leash

The most underrated release of the week. The number the FOMC watches most closely when deciding whether they can move.

University of Michigan Consumer Sentiment for March (preliminary) releases Friday morning. In most weeks it is a second-tier data point. This Friday it may be the most consequential single number of the entire week.

Here is why: the Federal Reserve has been explicit that it is monitoring longer-run inflation expectations to determine whether the public’s trust in the 2% target is holding. So long as 5-year expectations remain anchored below 3%, the Fed can frame an oil shock as a transient supply disruption and stay on hold without formally changing its guidance. The moment 5-year expectations break materially above 3%, the calculus shifts and the Fed must choose between growth and inflation in a way it has not had to since 2022.

January and February Michigan 5-year expectations were already running at 3.1-3.3%. Gas prices rose nearly 27 cents in the week following the strikes, the fastest weekly jump since March 2022. Consumer inflation expectations tend to be heavily anchored to petrol prices at the pump. The March preliminary Michigan survey captures respondents filling their tanks at $3.25+ national average gas.

This is the mechanism through which the oil shock constrains the Fed, regardless of what core CPI prints. If Michigan expectations re-accelerate above 3.3%, every Fed speaker who has been maintaining a “wait and see” posture faces discomfort.

Below 3.3%: Fed can maintain hold posture, frame oil as transient. Above 3.3%: expectations de-anchoring narrative gains traction, cuts formally delayed through year-end. Above 3.5%: the 2022 playbook resurfaces and rate hikes re-enter market pricing.

The Daily Variables: Oil and Tanker Traffic

Whatever the official data prints, Brent and tanker traffic will be giving you a live read on the regime all week. Here is how to use them.

Brent: The Regime Barometer

Issue #013’s signpost was $85. Brent closed Friday at $92.69 and are currently tracking $100+. The question for this week is not whether the shock is real, it is and it is deepening, but whether it is beginning to resolve or continuing to escalate. These are the levels that carry regime meaning from here:

• Below $95 mid-week: De-escalation signal being priced. A move back below the Friday close from the Monday open gap would indicate the market is pricing a diplomatic resolution faster than the physical disruption suggests. Treat with scepticism until tanker traffic confirms.

• $95-105 range: Holding pattern. Shock priced in, no resolution visible. Path B persists. CPI and claims data become the dominant regime variable.

• Above $110 sustained: Escalation pricing accelerating. Gulf storage constraints becoming production constraints. JPMorgan’s 4mb/d production cut scenario begins to materialise. Stagflation deepens - Growth pillar risks moving to -3.

Tanker Traffic: The Physical Reality Check

Brent prices reflect market expectations. Tanker traffic through Hormuz reflects physical reality. Vortexa and Lloyd’s List data have been the most reliable leading indicator of whether the disruption is easing or deepening.

Pre-shock baseline was 24 vessels per day. At the lowest point this week it was effectively zero, three vessels, all Iran-flagged. The $20 billion US insurance program and naval escort offer have not restored commercial traffic. Watch this number daily. Any sustained recovery toward 10+ vessels would be the first concrete de-escalation signal that the market, and the framework, would need to price.

Cross-Asset Positioning: How Each Asset Class Reads the Week

Path B is the operating framework. Here is how each asset class is positioned heading into the week’s data and what changes the thesis.

Equities — VIX above 30, Rotation Underway

S&P at 6,670, down from 6,879 pre-shock. Russell 2000 underperforming at 2,484, consistent with a Stagflation move where tight-margin domestic names feel the squeeze first as input costs rise and growth expectations fall. VIX above 30 is elevated but not yet at stress levels; the 2022 peak saw 36+. The index-level decline is modest relative to the severity of the shock, which means either the market is pricing a quick resolution or the rotation pain is concentrated in sectors rather than visible at the headline level. Both can be true simultaneously.

A hot Wednesday CPI print will test the index level materially. Elevated VIX + rising inflation expectations + no Fed backstop is a combination equities have handled poorly historically.

Gold - Tactical Flush, Structural Bid Intact

Gold at $5,100 is below its pre-shock $5,200+ level. De-risking events typically produce short-term gold selling as investors raise cash across positions, this is mechanical. The structural thesis (central bank buying, real rate compression, dollar weakness, policy uncertainty) is not only intact but strengthened by the supply shock. Watch for gold to recover the pre-shock level once the mechanical selling clears. Stagflation is historically the strongest macro environment for gold.

Bonds - Competing Forces, Watch 2s10s

The 10Y at approximately 4.18% is caught between flight-to-safety demand (lower) and inflation repricing (higher). These forces are roughly balanced at current levels. Wednesday’s CPI breaks the tie. A hot print pushes the 10Y higher; a soft print allows the safety bid to dominate temporarily. The more strategically significant spread is 2s10s: steepening confirms the Stagflation read (growth deteriorating, inflation sticky, Fed frozen). Watch for that spread to break materially wider through the week, sustained steepening is how the bond market prices a regime that is simultaneously recessionary and inflationary.

Global Spillover - EM and Asia Carry the Largest Exposure

The 20% of global oil that moves through Hormuz is not evenly distributed. China, India, Japan and South Korea collectively account for roughly three-quarters of the flows behind the strait. Japan sources 70% of its Middle Eastern crude through Hormuz; Japanese refiners have already asked their government to release strategic reserves. India has approximately two months of import coverage; Thailand has moved to ban fuel exports. These are not tail scenarios, they are current policy responses to a physical supply shock that is landing hardest in Asia.

For the regime framework, the EM/Asia dimension adds two risks that are not fully visible in the US data: currency stress (oil-importing EM currencies under pressure as dollar demand rises and import bills surge) and a demand destruction feedback loop if the shock is severe enough to materially slow Asian growth. Neither is this week’s primary variable, but both belong in the cross-asset picture for any reader with international exposure.

FX - Dollar Finds the Bid It Lacked

DXY has recovered to 99+, finding safe-haven demand after months of structural weakness below 100. This is a regime-consistent response: geopolitical shocks bid dollars in the near term. The structural weakness thesis (DXY as a signpost) is being tested but not broken. USD/JPY, the persistent carry risk signpost since Issue #001 — becomes more dangerous as Japanese investors repatriate assets in a risk-reduction environment. The carry unwind risk that sat unresolved for fourteen weeks is now in a higher-stress context. Watch USD/JPY, a break lower means the carry unwind could be in motion.

The Bottom Line

The regime has moved to Stagflation. The data (even the backwards-looking data from February) was already building that case before Brent hit $100. ISM Prices Paid at 70.5. NFP -92,000. Core PCE at 2.9%. Unemployment rising. These were the numbers before a barrel of Hormuz disruption reached a consumer. The Tearsheet has scored this unambiguously: Growth deeply negative, Inflation elevated, Policy trapped. Stagflation is the confirmed call.

This week, the framework gets its first genuine forward-looking data under the new conditions. Wednesday’s CPI tells us the floor. Thursday’s claims tell us whether hiring decisions have changed. Friday’s Michigan expectations tell us whether the Fed can maintain its holding pattern or whether the policy trap becomes unavoidable.

The most important thing to understand about this week: the data will still be largely backwards-looking but the market is pricing forward. That gap between what the official statistics show and what the oil market is already pricing is where the regime analysis has to operate. The framework is designed for exactly this: to read the leading signals (Brent, tanker traffic, expectations) before they show up in the lagged statistics.

Watch oil. Watch the Michigan expectations number. Know what each one means for the regime before it prints. The week that follows will be a lot clearer if the framework is set up before Tuesday’s open.

Questions or feedback? macroanalytix.research@gmail.com

Disclaimer

All content published by MacroAnalytix is for research and educational purposes only. Nothing in this publication constitutes financial advice, investment recommendations, or solicitation to buy or sell any securities. The regime framework and cross-asset analysis represent the author’s interpretation of publicly available data and should not be relied upon as the sole basis for investment decisions. Past performance of the framework or any referenced positioning ideas does not guarantee future results. Always consult a qualified financial advisor before making investment decisions. MacroAnalytix and TMS Capital are complementary but distinct entities.