What’s Happening

If you’ve spent five minutes on FinTwit today, you already know: NVIDIA either saves civilization after the close tonight or we’re all bartering canned goods by Friday. The S&P is either going to 10,000 or the economy ceases to exist. There is, apparently, no middle ground.

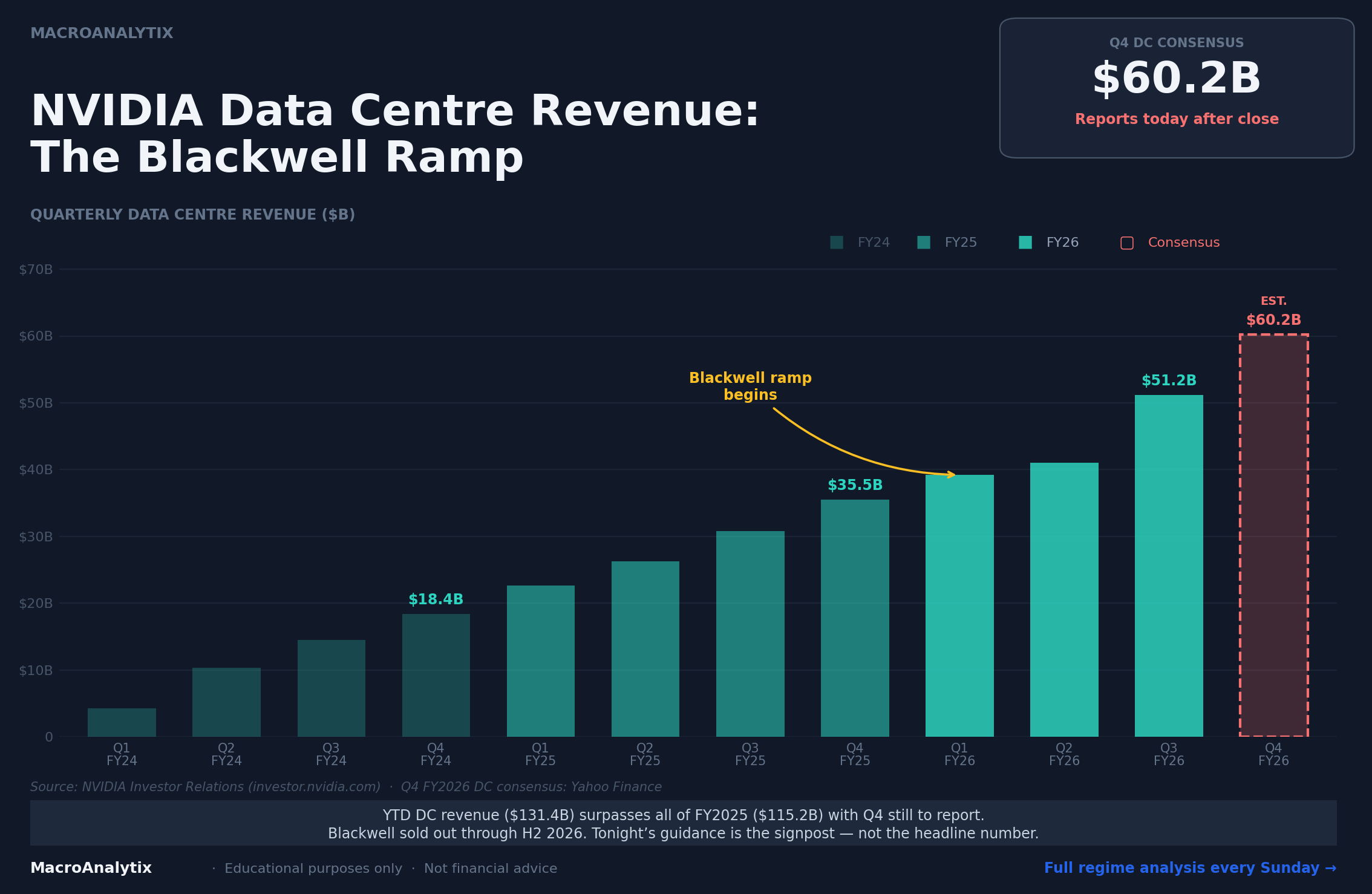

Back in reality: NVIDIA reports fourth-quarter earnings after the bell. The Street expects $65.7 billion in revenue and $1.52 in earnings per share, both records. But this isn’t about whether they beat. They’ve beaten in sixteen of the last eighteen quarters. The real event is what they say about the next twelve months and whether the AI capex supercycle that’s been propping up growth, risk appetite and index-level returns still has legs.

The Regime Implications

Forget the stock for a moment. Think about what NVIDIA’s numbers actually tell us about the regime.

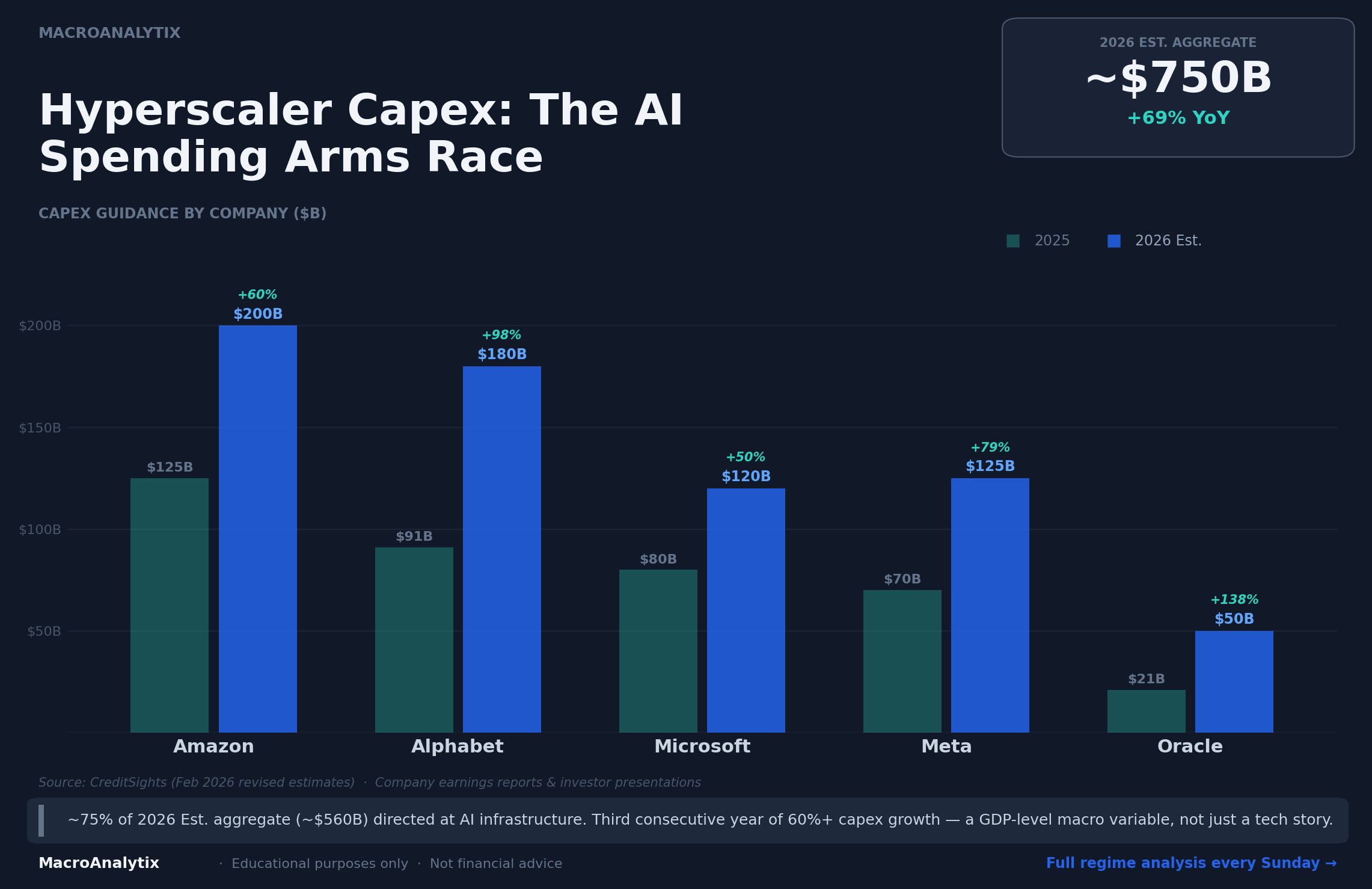

Growth pillar: Hyperscaler capex has been one of the few bright spots keeping business investment alive while housing stagnates and manufacturing grinds. Combined Big Five capex guidance for 2026 has ballooned to roughly $750 billion, up from ~$443 billion in 2025, a 69% year-over-year increase and the third consecutive year of 60%+ growth. If NVIDIA’s guidance signals that spending is accelerating, the growth pillar gets a tailwind that offsets weakness elsewhere. If it signals deceleration, the one engine that’s been working starts to sputter.

The catalyst behind the spending: Blackwell. NVIDIA’s next-generation platform is sold out through the back half of 2026 with billions already booked in its first quarter of availability. The Meta partnership announced this month included millions of Blackwell and Rubin GPUs under a multi-year deal and underscores the demand visibility. If tonight’s call confirms that the Blackwell ramp is on track with no yield or supply issues, it validates the capex cycle. If there are production hiccups, it gives the efficiency bears something to point at.

Risk Appetite pillar: NVIDIA is roughly 7% of the S&P 500. When a single stock commands that kind of index weight, its earnings become a risk appetite event. The concentration problem cuts both ways. A strong print keeps the mag-7 engine running and flattens any breadth concerns. A disappointing guide exposes just how narrow the rally has been. The stock’s been sideways for three to six months, which suggests expectations aren’t euphoric. That’s actually constructive and leaves room for a positive surprise to matter.

The So What

For the regime framework, there are two scenarios that matter and one that doesn’t:

Scenario A: Guidance accelerates. Q1 FY2027 guide comes in above the $65 billion whisper number. Gross margins hold mid-70s. Blackwell demand visibility extends through calendar 2027. This reinforces the AI capex supercycle narrative and keeps the Growth and Risk Appetite pillars supported. The regime stays Neutral/Chop with upward pressure. It’s not a regime shift, but it removes a downside catalyst and gives Sunday’s Setup a more constructive tone.

Scenario B: Guidance disappoints. Revenue guide below $60 billion or margin compression below 70%. This is the DeepSeek thesis playing out. Efficiency gains reducing the brute-force compute demand that NVIDIA has monetised. It would pressure Risk Appetite directly through index impact and raise questions about the sustainability of the capex cycle that’s been supporting Growth. That’s regime-relevant. If this happens, expect a Regime Alert before Sunday.

Scenario C: In-line beat, vague guidance. This is the most likely outcome and the least interesting. Revenue beats by a billion or two, guidance roughly matches, stock moves a few percent either way and settles. The regime doesn’t change. Sunday’s Setup addresses it in the Risk Appetite section and moves on.

The Signpost

Skip the headline revenue number, everyone will have that within seconds. Here’s what to listen for:

Data centre revenue composition. Last quarter it was $51.2 billion with networking more than doubling. If networking revenue growth decelerates sharply, the infrastructure buildout may be further along than bulls think. If it re-accelerates, the capex cycle has another leg.

Gross margin trajectory. Mid-70s is the line. Jensen guided 75% non-GAAP last quarter. If that slips below 72%, it signals competition or pricing pressure from the efficiency argument. Margins tell you more about NVIDIA’s moat than revenue does.

The China commentary. Revenue from China was essentially zero last quarter after export restrictions killed H20 demand. Any change in tone here matters for geopolitical risk pricing and for the broader tech cold war narrative that feeds into Policy.

Results drop at 5pm Eastern. If they’re regime-material, you’ll hear from me before Sunday. If they’re not, we’ll fold it into The Setup and keep moving.

Questions or feedback? macroanalytix.research@gmail.com

Disclaimer

All content published by MacroAnalytix is for research and educational purposes only. Nothing on this site or in our publications should be interpreted as financial advice, investment recommendations, or a solicitation to buy or sell securities. You are solely responsible for your own financial decisions. Please conduct your own due diligence and consult with a licensed financial professional before making any investment decisions.